Medicare vs Medicaid is one of the most frequently asked questions families encounter when planning for healthcare, aging, and long-term care. Although the programs have similar names, they serve different purposes and cover different types of services.

Medicare is a federal health insurance program primarily for adults age 65 and older, as well as certain younger individuals with disabilities. Medicaid is a joint federal and state program that provides healthcare coverage and long-term care assistance for eligible individuals who meet income and financial requirements.

While Medicare generally helps pay for hospital care, physician services, preventive care, prescription medications, and short-term rehabilitation, Medicaid is the primary payer of long-term nursing home care and many other long-term care services in the United States.

Understanding the difference between Medicare and Medicaid can help families avoid costly surprises, better prepare for future care needs, and make more informed decisions about assisted living, memory care, home health care, nursing homes, hospice care, and long-term care planning.

Quick Answer: What Is the Difference Between Medicare and Medicaid?

Medicare is primarily a health insurance program for older adults and certain individuals with disabilities, regardless of income. Medicaid is a healthcare and long-term care assistance program for eligible individuals who meet financial requirements. While Medicare generally covers medical care and short-term rehabilitation, Medicaid often helps pay for long-term care services, including nursing home care and certain home and community-based supports.

Who Should Read This Guide?

This guide is designed for anyone trying to understand the differences between Medicare and Medicaid, especially if you are planning for future healthcare or senior care needs.

This guide may be helpful if you are:

- An adult approaching Medicare eligibility and preparing for retirement

- A family caregiver helping a parent, spouse, or loved one understand healthcare coverage

- Exploring assisted living, memory care, home health care, nursing homes, hospice care, or other long-term care services

- Planning ahead for future healthcare and long-term care costs

- Trying to understand what Medicare and Medicaid do—and do not—cover

- Looking for ways to pay for long-term care while protecting your financial future

- Feeling confused about Medicare, Medicaid, or how the two programs work together

Whether you are planning ahead or facing an immediate care decision, this guide will help you better understand your options so you can make more informed decisions with confidence.

Table of Contents

Why Families Often Confuse Medicare and Medicaid

Although Medicare and Medicaid have similar names, they are separate programs with different eligibility requirements, benefits, and purposes. Medicare is primarily a health insurance program for older adults and certain individuals with disabilities, while Medicaid provides healthcare coverage and long-term care assistance for eligible individuals based largely on income and financial need.

The confusion often arises because both programs help pay for healthcare services, and some individuals qualify for both Medicare and Medicaid at the same time. In addition, families frequently begin researching both programs when a loved one needs assisted living, memory care, home health care, nursing home care, or other long-term care services.

Understanding how Medicare and Medicaid differ, and how they may work together, can help families make more informed decisions about healthcare coverage, long-term care planning, and future financial needs.

Understanding Medicare vs Medicaid

When an older adult begins needing additional support, many families assume Medicare will cover all healthcare and long-term care expenses. Unfortunately, that is one of the most common misconceptions about senior care.

Understanding Medicare vs Medicaid becomes especially important when exploring care options such as:

Although the names sound similar, Medicare and Medicaid are separate programs with different eligibility requirements, benefits, and coverage limitations. Medicare primarily helps pay for healthcare services, while Medicaid often plays a critical role in covering long-term care for eligible individuals.

Knowing how each program works can help families avoid unexpected costs, plan more effectively for future care needs, and make informed decisions about the type of care and support a loved one may need as they age.

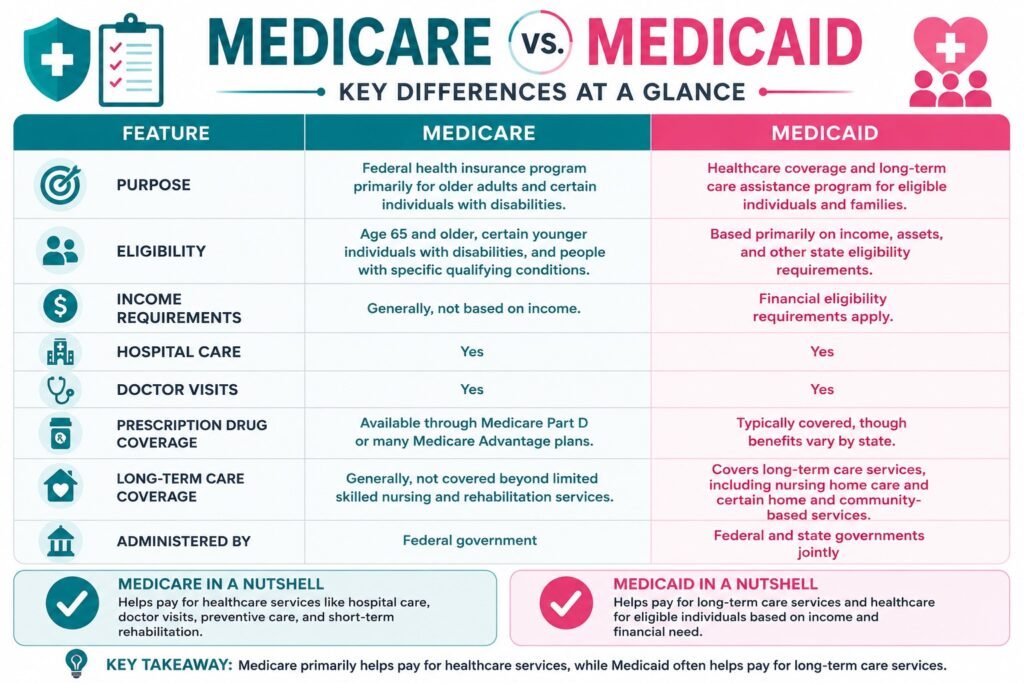

Medicare vs Medicaid: Side-by-Side Comparison

| Feature | Medicare | Medicaid |

| Purpose | Federal health insurance program primarily for older adults and certain individuals with disabilities | Healthcare coverage and long-term care assistance program for eligible individuals and families |

| Primary Eligibility | Age 65 and older, certain younger individuals with disabilities, and people with specific qualifying conditions | Based primarily on income, assets, and other state eligibility requirements |

| Income Requirements | Generally, not based on income | Financial eligibility requirements apply |

| Monthly Premiums | Often required for certain parts of Medicare | Usually, low cost or no cost for eligible individuals |

| Hospital Coverage | Yes | Yes |

| Doctor Visits | Yes | Yes |

| Prescription Drug Coverage | Available through Medicare Part D or many Medicare Advantage plans | Typically covered, though benefits vary by state |

| Preventive Care | Yes | Yes |

| Short-Term Rehabilitation | Yes, when eligibility requirements are met | Yes |

| Long-Term Nursing Home Care | Generally, not covered beyond limited skilled nursing and rehabilitation services | Covered for eligible individuals |

| Assisted Living Coverage | Generally, not covered | May help cover certain care services through state waiver programs |

| Memory Care Coverage | Covers medical services related to dementia but not long-term residential memory care | May help cover long-term memory care services for eligible individuals |

| Home Health Care | Covers certain medically necessary home health services | May cover a broader range of home and community-based services |

| Long-Term Personal Care Assistance | Generally, not covered | Often covered for eligible individuals |

| Administered By | Federal government | Federal and state governments jointly |

Key Takeaway

The biggest difference between Medicare and Medicaid is that Medicare primarily helps pay for healthcare services, while Medicaid often helps pay for long-term care services. This distinction becomes especially important when families are exploring nursing homes, memory care, assisted living, home health care, or other long-term care options.

What Is Medicare?

Medicare is a federal health insurance program designed primarily for adults age 65 and older, as well as certain younger individuals with disabilities and people with specific qualifying medical conditions.

Most Americans become eligible for Medicare when they turn 65, regardless of income. Unlike Medicaid, Medicare eligibility is generally not based on financial need. Families can find detailed information about eligibility, enrollment, and coverage through Medicare.gov, the official Medicare resource for beneficiaries and caregivers.

Medicare helps cover a wide range of healthcare services, including hospital care, physician visits, preventive care, prescription medications, and certain short-term rehabilitation services. However, Medicare was designed primarily to provide health insurance coverage and generally does not cover most long-term custodial care services.

Understanding what Medicare does and does not cover is an important part of planning for future healthcare and long-term care needs.

Medicare Part A (Hospital Insurance)

Medicare Part A helps cover inpatient and facility-based care, including:

- Hospital stays

- Skilled nursing facility rehabilitation following a qualifying hospital stay

- Hospice care

- Certain home health services

Part A is often referred to as hospital insurance because it primarily covers care received in healthcare facilities rather than routine medical services.

Medicare Part B (Medical Insurance)

Medicare Part B helps cover outpatient and medically necessary services, including:

- Physician visits

- Preventive screenings and wellness visits

- Outpatient care

- Diagnostic testing and laboratory services

- Durable medical equipment

- Certain therapies and treatments

Together, Medicare Parts A and B are commonly referred to as Original Medicare.

Medicare Part C (Medicare Advantage)

Medicare Advantage plans are offered through private insurance companies approved by Medicare.

These plans provide the same basic coverage as Original Medicare and may also include additional benefits such as:

- Hospital coverage

- Medical coverage

- Prescription drug coverage

- Dental benefits

- Vision benefits

- Hearing benefits

- Wellness and fitness programs

Benefits, provider networks, and costs vary by plan and location.

Medicare Part D (Prescription Drug Coverage)

Medicare Part D helps cover the cost of prescription medications.

Part D plans are offered through private insurance companies and can help reduce out-of-pocket medication expenses. Coverage, formularies, and costs vary depending on the plan selected.

What Is Medicaid?

Medicaid is a public health insurance program jointly funded by federal and state governments that helps provide healthcare coverage and long-term care assistance for eligible individuals and families.

Unlike Medicare, which is primarily based on age or disability status, Medicaid eligibility is largely determined by income, assets, and other financial criteria established by each state. Because states administer their own Medicaid programs within federal guidelines, eligibility requirements, covered services, and available benefits can vary across the country. Families can find state-specific information about eligibility, benefits, and long-term care services through Medicaid.gov.

Medicaid provides healthcare coverage for millions of Americans, including:

- Older adults

- Individuals with disabilities

- Children

- Pregnant women

- Low-income adults and families

For many seniors, Medicaid becomes especially important when ongoing long-term care services are needed. In fact, Medicaid is the primary payer of long-term nursing home care in the United States and may also help cover certain home and community-based services, personal care assistance, and other long-term care supports for eligible individuals.

What Is the Difference Between Medicare and Medicaid?

The biggest difference between Medicare and Medicaid is their purpose and the types of services they are designed to cover.

Medicare is primarily a health insurance program that helps pay for medical care, hospital services, preventive care, and short-term rehabilitation. Eligibility is generally based on age or disability status rather than income.

Medicaid is a healthcare and long-term care assistance program that helps eligible individuals access medical services as well as certain long-term care supports. Eligibility is largely based on income, assets, and other financial requirements established by each state.

In general, Medicare focuses on:

- Medical treatment

- Hospital care

- Physician services

- Preventive care

- Prescription medications

- Short-term rehabilitation

Medicaid often helps pay for:

- Long-term nursing home care

- Personal care assistance

- Home and community-based services

- Certain assisted living services through state programs

- Long-term support for individuals with chronic health conditions or disabilities

For many families, the most important distinction is that Medicare primarily helps pay for healthcare services, while Medicaid is often the program that helps pay for long-term care services when ongoing support is needed.

Understanding this difference becomes increasingly important as care needs change with age and families begin exploring options such as home health care, assisted living, memory care, nursing homes, or hospice care.

Does Medicare Pay for Long-Term Care?

One of the most common misconceptions about Medicare is that it pays for long-term care. In reality, Medicare was designed primarily to cover healthcare services, not ongoing custodial care.

In most situations, Medicare does not cover long-term care when the primary need is assistance with everyday activities such as:

- Bathing

- Dressing

- Eating

- Toileting

- Mobility and transferring

- Medication reminders

- Supervision related to Alzheimer’s disease or other forms of dementia

These types of services are often referred to as custodial care or personal care, and they are commonly provided in assisted living communities, memory care communities, residential care homes, and nursing homes.

Medicare may cover short-term skilled nursing care, rehabilitation services, and certain home health services when specific eligibility requirements are met, such as following a qualifying hospital stay. However, Medicare generally does not pay for permanent residence in a nursing home, long-term personal care assistance, or ongoing supervision related to chronic health conditions or cognitive decline.

This distinction is often one of the biggest surprises families encounter when planning for future care needs. Many people assume Medicare will cover all senior care expenses, only to discover that long-term care services are typically paid for through personal funds, long-term care insurance, veterans’ benefits, Medicaid, or a combination of resources.

Understanding what Medicare does and does not cover can help families plan ahead, explore available financial resources, and avoid unexpected costs as care needs change over time.

To learn more, read our article Long-Term Care Explained: A Complete Guide for Families Navigating Senior Care.

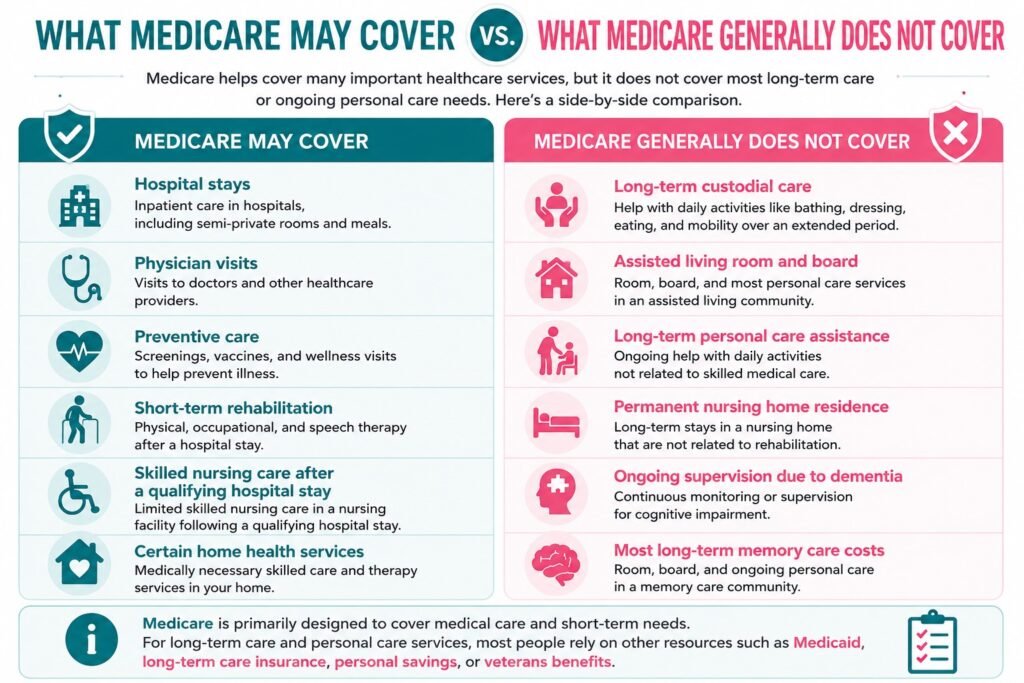

What Medicare May Cover vs. What Medicare Generally Does Not Cover

| Medicare May Cover | Medicare Generally Does Not Cover |

| Hospital stays | Long-term custodial care |

| Physician visits | Assisted living room and board |

| Preventive care | Long-term personal care assistance |

| Short-term rehabilitation | Permanent nursing home residence |

| Skilled nursing care after a qualifying hospital stay | Ongoing supervision due to dementia |

| Certain home health services | Most long-term memory care costs |

How Medicaid Helps Pay for Long-Term Care

Medicaid is the largest public payer of long-term care services in the United States and plays a critical role in helping eligible individuals access care when ongoing support is needed. According to the Centers for Medicare & Medicaid Services, Medicaid helps fund long-term services and supports, including nursing home care and certain home and community-based services.

For many older adults, Medicaid becomes especially important when long-term care expenses exceed personal financial resources. Unlike Medicare, which primarily covers healthcare services and short-term rehabilitation, Medicaid may help cover a variety of long-term care services for individuals who meet financial and eligibility requirements.

Depending on the state and specific program, Medicaid may help cover:

- Long-term nursing home care

- Personal care assistance

- Home health services

- Adult day programs

- Certain memory care services

- Home and Community-Based Services (HCBS)

- Assistance that helps older adults remain in their homes or communities longer

Many states offer programs designed to help eligible individuals receive care in home and community settings rather than moving directly into a nursing home. These programs can provide valuable support for older adults who need assistance with daily activities while maintaining as much independence as possible.

Because Medicaid programs are administered by individual states, coverage, available services, and eligibility requirements vary across the country. Families should review their state’s Medicaid program to better understand available benefits and qualification guidelines.

Medicaid Eligibility Varies by State

Although Medicaid is a federal and state program, eligibility requirements, income limits, asset limits, and available long-term care services can vary significantly from one state to another. Some states offer expanded home and community-based services, while others may have different eligibility pathways for long-term care assistance.

Families should review their state’s Medicaid guidelines or speak with a qualified benefits specialist to better understand available programs and determine whether a loved one may qualify for assistance. Understanding eligibility requirements early can help families plan ahead and avoid delays when long-term care services become necessary.

Why Medicaid Matters for Long-Term Care Planning

As care needs increase with age, many families discover that Medicare alone may not cover the ongoing support a loved one requires. Understanding how Medicaid works—and whether a loved one may qualify—can be an important part of planning for future care needs, managing long-term care costs, and exploring available care options.

For many families, Medicaid ultimately becomes one of the most important resources available for helping pay for long-term nursing home care, personal care services, and other long-term supports that may be needed as a loved one ages.

Medicare vs Medicaid for Assisted Living

Families frequently ask whether Medicare or Medicaid will help pay for assisted living. Understanding the differences between the two programs can help families plan more effectively and avoid unexpected costs.

Medicare and Assisted Living

Medicare generally does not cover assisted living costs because assisted living is considered a residential and custodial care service rather than medical care. In most situations, Medicare does not cover:

- Assisted living room and board

- Personal care assistance

- Help with activities of daily living

- Long-term custodial care

However, Medicare may continue to cover certain healthcare services received while living in an assisted living community, such as physician visits, hospital care, rehabilitation services, prescription medications, and eligible home health services.

Medicaid and Assisted Living

Medicaid coverage for assisted living varies by state.

Some states offer Home and Community-Based Services (HCBS) waiver programs that may help cover certain care-related services provided within assisted living communities. Depending on the program, Medicaid may help pay for services such as:

- Personal care assistance

- Medication management

- Care coordination

- Support with activities of daily living

However, Medicaid generally does not cover room and board costs in assisted living communities, meaning residents are often responsible for housing and meal expenses.

Because Medicaid programs differ across the country, families should review their state’s eligibility requirements and available waiver programs to determine what benefits may be available.

What Families Should Know

Many families are surprised to learn that neither Medicare nor Medicaid typically covers the full cost of assisted living. As a result, assisted living is often paid for through a combination of personal savings, retirement income, long-term care insurance, veterans’ benefits, and, in some cases, Medicaid waiver programs.

If your family is considering assisted living, our Questions to Ask When Touring Assisted Living Communities: Helpful Tips for Families guide offers practical tips and essential questions to help you evaluate communities, compare your options, and choose the best fit for your loved one.

Medicare vs Medicaid for Residential Care Homes

Residential care homes provide housing, personal care, supervision, and daily support in a smaller, home-like setting. These communities are often designed for older adults who need assistance with daily activities but do not require intensive medical care.

Families frequently ask whether Medicare or Medicaid will help pay for residential care home services.

Medicare and Residential Care Homes

Medicare generally does not cover the cost of living in a residential care home. In most situations, Medicare does not pay for:

- Room and board

- Personal care assistance

- Supervision and daily support

- Long-term custodial care

However, Medicare may continue to cover eligible healthcare services received while residing in a residential care home, including physician visits, hospital care, prescription medications, rehabilitation services, and certain home health services.

Medicaid and Residential Care Homes

Medicaid coverage for residential care homes varies by state. Depending on the state and available programs, Medicaid may help cover certain care-related services provided in residential care homes, such as:

- Personal care assistance

- Medication management

- Support with activities of daily living

- Care coordination

- Certain long-term care services

However, room and board costs are often not fully covered, and benefits can vary significantly by state and program.

What Families Should Know

Many residential care homes are paid for through a combination of personal savings, retirement income, long-term care insurance, veterans’ benefits, and, in some cases, Medicaid assistance programs.

Because coverage rules vary, families should speak with individual providers and review their state’s Medicaid programs to better understand available benefits and potential out-of-pocket costs.

To learn more about this care option, see our Residential Care Homes for Seniors: A Complete Guide for Families.

Medicare vs Medicaid for Memory Care

Memory care communities provide specialized support for individuals living with Alzheimer’s disease and other forms of dementia. These communities are designed to provide a safe environment, structured routines, specialized staff training, and assistance with daily activities while supporting residents’ cognitive and emotional well-being.

One of the most common questions families ask is whether Medicare or Medicaid will help pay for memory care services.

Medicare and Memory Care

Medicare may help cover healthcare services related to dementia and memory loss, including:

- Physician visits

- Hospital care

- Medical treatment

- Diagnostic testing

- Prescription medications

- Short-term rehabilitation services

- Certain home health services

However, Medicare generally does not cover the long-term residential costs associated with memory care communities. While Medicare may continue to pay for eligible medical services received by a resident, it typically does not pay for housing, supervision, personal care assistance, or ongoing dementia-related support provided in a memory care setting.

Medicaid and Memory Care

Depending on eligibility requirements and available state programs, Medicaid may help cover certain long-term memory care services. Coverage varies by state but may include:

- Long-term nursing home care

- Personal care assistance

- Specialized dementia support services

- Home and Community-Based Services (HCBS)

- Certain memory care-related services through approved programs

Because Medicaid programs differ across the country, families should review their state’s eligibility requirements and available benefits to determine what types of memory care support may be covered.

What Families Should Know

Memory care is often paid for through a combination of personal funds, long-term care insurance, veterans’ benefits, Medicaid, and other available financial resources. Understanding what Medicare and Medicaid do, and do not, cover can help families plan ahead and avoid unexpected expenses as care needs progress.

Families researching dementia care and support options may also find our Memory Care Explained guide helpful for understanding services, costs, and when specialized memory care may be appropriate.

Medicare vs Medicaid for Nursing Home Care

Nursing home care is one of the areas where the differences between Medicare and Medicaid become most significant. Understanding how each program works can help families better prepare for the financial realities of long-term care.

Medicare and Nursing Home Care

Medicare may help cover certain short-term nursing home services when specific eligibility requirements are met. Medicare may cover:

- Short-term rehabilitation services

- Skilled nursing care following a qualifying hospital stay

- Physical, occupational, and speech therapy

- Certain medically necessary treatments and services

However, Medicare generally does not cover:

- Long-term nursing home residence

- Ongoing custodial care

- Assistance with activities of daily living when no skilled medical care is required

- Permanent long-term care in a nursing home setting

Coverage is typically limited to short-term recovery and rehabilitation rather than ongoing long-term support.

Medicaid and Nursing Home Care

For eligible individuals, Medicaid may help cover the cost of long-term nursing home care. Depending on eligibility requirements and state regulations, Medicaid may help pay for:

- Long-term nursing home residence

- Personal care assistance

- Room and board in Medicaid-certified nursing facilities

- Ongoing supervision and support

- Medical and personal care services provided within the facility

Because nursing home care can be expensive, Medicaid often becomes an important resource for older adults who require long-term care and meet financial eligibility requirements.

What Families Should Know

Many families are surprised to learn that Medicare generally covers short-term rehabilitation, while Medicaid is often the program that helps pay for ongoing nursing home care.

As care needs increase and personal financial resources become limited, some older adults eventually qualify for Medicaid to help cover long-term nursing home expenses. Understanding these differences can help families plan ahead, explore available financial resources, and make more informed decisions about future care needs.

To learn more about services, levels of care, and when nursing home care may be appropriate, read our What Is a Nursing Home? A Complete Guide for Families Navigating Skilled Nursing Care.

Medicare vs Medicaid for Home Health Care

Home health care can help older adults receive care and support while remaining in their homes. Depending on an individual’s needs, home health care may include skilled medical services, rehabilitation therapies, personal care assistance, or a combination of supports.

Understanding how Medicare and Medicaid cover home health care can help families better plan for care at home and avoid unexpected expenses.

Medicare and Home Health Care

Medicare may cover certain medically necessary home health services when specific eligibility requirements are met. Depending on the situation, Medicare may help cover:

- Skilled nursing care

- Physical therapy

- Occupational therapy

- Speech therapy

- Medical social services

- Certain home health aide services related to a covered healthcare plan

However, Medicare generally does not cover ongoing personal care assistance when that is the primary service needed. Long-term help with bathing, dressing, meal preparation, housekeeping, and other non-medical support services is typically not covered.

Medicaid and Home Health Care

Medicaid may provide a broader range of home-based support services for eligible individuals, although benefits vary by state. Depending on the program, Medicaid may help cover:

- Personal care assistance

- Home health aide services

- Skilled nursing services

- Support with activities of daily living

- Home and Community-Based Services (HCBS)

- Certain caregiver support services

Many state Medicaid programs are designed to help older adults remain safely at home for as long as possible rather than moving into a residential care setting.

What Families Should Know

One of the biggest differences between Medicare and Medicaid is that Medicare primarily covers medically necessary healthcare services, while Medicaid may help cover both healthcare and long-term personal care support for eligible individuals.

As a result, many families use a combination of Medicare, Medicaid, private insurance, long-term care insurance, veterans’ benefits, and personal funds to help pay for care at home.

Medicare vs Medicaid for Hospice Care

Hospice care provides comfort-focused support for individuals facing a life-limiting illness when the focus of care shifts from curative treatment to quality of life, comfort, and symptom management.

Understanding how Medicare and Medicaid cover hospice services can help families make informed decisions during a difficult and emotional time.

Medicare and Hospice Care

Medicare may cover hospice care through the Medicare Hospice Benefit when eligibility requirements are met. Medicare hospice coverage may include:

- Physician services

- Nursing care

- Medications related to symptom management and comfort

- Medical equipment and supplies

- Social work services

- Spiritual counseling

- Bereavement support for families

- Short-term respite care

Hospice services may be provided in a person’s home, an assisted living community, a residential care home, a nursing home, or a dedicated hospice facility.

Medicaid and Hospice Care

Medicaid also covers hospice services in most states for eligible individuals. Depending on the state and individual circumstances, Medicaid may help cover:

- Hospice care services

- Nursing services

- Medications related to the terminal illness

- Medical equipment and supplies

- Additional supportive services

For individuals receiving hospice care in a nursing home or other long-term care setting, Medicaid may also help cover certain long-term care costs that Medicare does not cover.

What Families Should Know

Unlike assisted living, memory care, and long-term nursing home care, hospice care is one of the areas where both Medicare and Medicaid may provide significant coverage for eligible individuals.

Because coverage requirements and benefits can vary, families should review their specific Medicare or Medicaid plan and speak with care providers to better understand available hospice services.

To learn more about hospice services and when hospice may be appropriate, see our Hospice Care Explained guide.

Can You Have Medicare and Medicaid at the Same Time?

Yes. Some individuals qualify for both Medicare and Medicaid. These individuals are often referred to as dual eligibles or dual-eligible beneficiaries.

Dual eligibility typically occurs when someone qualifies for Medicare based on age or disability and also meets their state’s Medicaid income and financial eligibility requirements.

For eligible individuals, having both programs can provide broader coverage and help reduce out-of-pocket healthcare expenses.

How Medicare and Medicaid Work Together

When someone is enrolled in both programs, Medicare generally pays first for covered healthcare services.

Medicare Pays First

Medicare typically helps cover:

- Hospital stays

- Physician visits

- Medical treatment

- Preventive care

- Prescription medications through eligible plans

- Short-term rehabilitation services

Medicaid Pays Second

Depending on eligibility and state programs, Medicaid may help cover:

- Medicare premiums

- Deductibles

- Copayments and coinsurance

- Long-term nursing home care

- Personal care services

- Home and community-based services

- Additional healthcare and support services not fully covered by Medicare

What Families Should Know

For many older adults with limited income and resources, dual eligibility can provide valuable financial assistance and access to a wider range of healthcare and long-term care services.

Because eligibility requirements and available benefits vary by state, families should review their state’s Medicaid program or speak with a qualified benefits specialist to determine whether a loved one may qualify.

Dual eligibility can significantly reduce healthcare costs and may play an important role in helping older adults access the care and support they need while preserving limited financial resources.

How Families Typically Pay for Long-Term Care

Paying for long-term care is one of the biggest concerns families face when exploring care options for an aging loved one. Because care needs, care settings, and financial situations vary widely, there is rarely a one-size-fits-all solution.

Many families use a combination of resources to help pay for care, including:

- Personal savings

- Retirement income

- Long-term care insurance

- Veterans’ benefits

- Medicare

- Medicaid

- Family contributions and other financial resources

The funding source often depends on the type of care needed. For example, Medicare may help cover certain healthcare services and short-term rehabilitation, while Medicaid may help cover long-term nursing home care and other long-term support services for eligible individuals.

Some families begin by paying privately and later explore Medicaid eligibility if care needs increase and financial resources become limited. Others may rely on long-term care insurance or veterans benefits to help offset costs.

Why Planning Ahead Matters

Long-term care needs often develop gradually, but the financial impact can be significant. Planning ahead gives families more time to understand available benefits, explore funding options, and make informed decisions before a healthcare crisis occurs.

Taking time to discuss care preferences, review financial resources, and learn how programs such as Medicare and Medicaid work can help reduce stress and preserve more care options in the future.

For additional guidance, see our article Senior Care Planning: How to Plan for Long-Term Care Before a Crisis Happens.

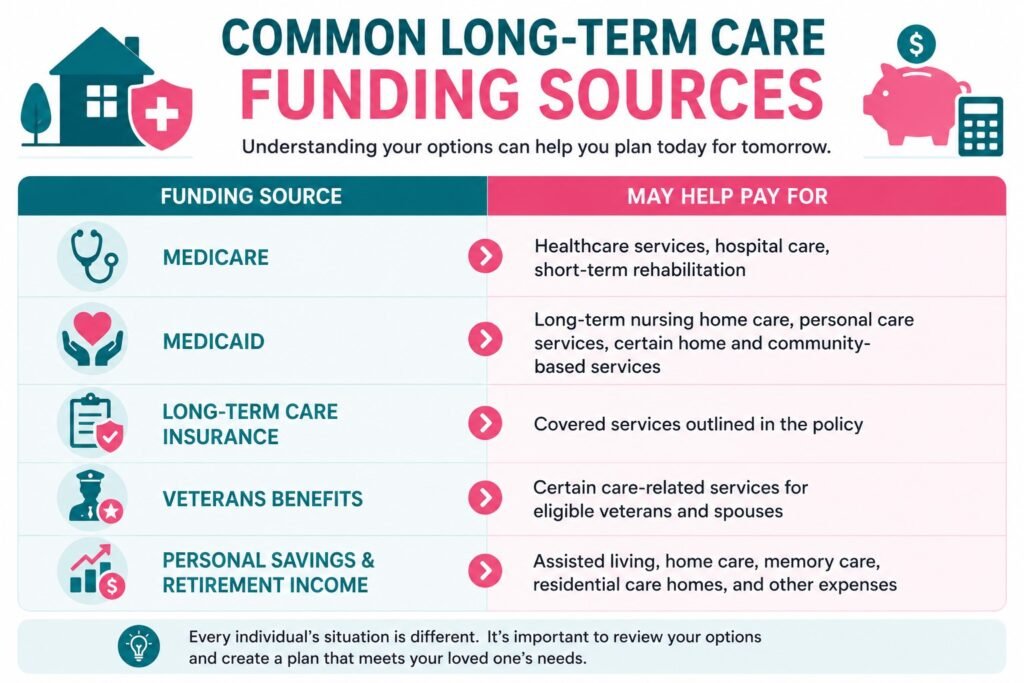

Common Long-Term Care Funding Sources

| Funding Source | May Help Pay For |

| Medicare | Healthcare services, hospital care, short-term rehabilitation |

| Medicaid | Long-term nursing home care, personal care services, certain home and community-based services |

| Long-Term Care Insurance | Covered services outlined in the policy |

| Veterans Benefits | Certain care-related services for eligible veterans and spouses |

| Personal Savings & Retirement Income | Assisted living, home care, memory care, residential care homes, and other expenses |

Signs It May Be Time to Explore Additional Care

Many families begin researching Medicare, Medicaid, and long-term care options after noticing changes in a loved one’s health, safety, or ability to manage daily activities independently.

While occasional challenges can be a normal part of aging, ongoing difficulties may indicate that additional support could improve quality of life and help reduce health and safety risks. The National Institute on Aging encourages families to pay attention to changes in mobility, memory, personal care, safety, and a person’s ability to manage everyday activities independently.

Common signs that it may be time to explore additional care include:

- Frequent falls or mobility concerns

- Difficulty managing medications

- Increasing memory loss or confusion

- Missed medical appointments

- Difficulty preparing meals or maintaining proper nutrition

- Challenges with bathing, dressing, or other personal care tasks

- Changes in hygiene or housekeeping

- Increased caregiver stress or burnout

- Difficulty managing chronic health conditions

Recognizing these signs early can give families more time to understand available care options, explore financial resources, and make informed decisions before a crisis occurs. Many families do not begin learning about Medicare, Medicaid, or long-term care funding until additional support is already needed. Starting the conversation early can help reduce stress, preserve more care options, and allow families to plan for future needs with greater confidence.

If you are concerned about a loved one’s changing needs, these resources may help:

- 12 Signs an Aging Parent May Need More Care

- When Is It Time for Assisted Living?

- Nursing Home vs Assisted Living: What’s the Difference? 7 Essential Facts Every Family Should Know

- Questions to Ask When Touring Nursing Homes: A Complete Guide for Families

- Hospital Discharge Planning for Seniors: Essential Steps to Choose the Right Care After a Hospital Stay

Frequently Asked Questions About Medicare vs Medicaid

Families researching Medicare and Medicaid often have questions about eligibility, coverage, costs, and long-term care services. Below are answers to some of the most frequently asked questions about Medicare vs Medicaid.

Is Medicare free at age 65?

Not always. While many people qualify for premium-free Medicare Part A based on their work history, Medicare Part B, Medicare Part D, and many Medicare Advantage plans may require monthly premiums. Deductibles, copayments, and coinsurance may also apply depending on the coverage selected.

Can someone have Medicare and Medicaid at the same time?

Yes. Individuals who qualify for both programs are known as dual eligibles. In many cases, Medicare serves as the primary payer for healthcare services, while Medicaid may help cover premiums, deductibles, copayments, long-term care services, and other eligible expenses.

What is the main difference between Medicare and Medicaid?

The primary difference is that Medicare is a health insurance program primarily for older adults and certain individuals with disabilities, while Medicaid is a healthcare and long-term care assistance program for people who meet financial eligibility requirements. Medicare focuses on healthcare services, while Medicaid often helps cover long-term care.

Does Medicare pay for long-term care?

Medicare generally does not cover long-term custodial care, assisted living, or permanent nursing home residence. Medicare may cover short-term rehabilitation and skilled nursing care under specific circumstances, but ongoing long-term care is often paid through personal funds, long-term care insurance, Medicaid, or other resources.

Does Medicare pay for assisted living?

Generally, no. Medicare does not typically cover assisted living room and board, personal care assistance, or long-term custodial care. However, Medicare may continue to cover eligible medical services received while living in an assisted living community.

Does Medicaid cover assisted living?

In some states, Medicaid waiver programs may help cover certain care-related services provided in assisted living communities. However, room and board costs are often not covered.

Does Medicare pay for nursing home care?

Medicare may cover short-term skilled nursing care and rehabilitation following a qualifying hospital stay. However, Medicare generally does not cover long-term nursing home residence or ongoing custodial care.

Does Medicaid pay for nursing homes?

Yes. Medicaid is the primary payer of long-term nursing home care in the United States for eligible individuals who meet financial and medical eligibility requirements.

Does Medicare cover memory care?

Medicare may cover medical services related to dementia, including physician visits, hospital care, and certain treatments. However, Medicare generally does not cover the long-term residential costs associated with memory care communities.

Does Medicare cover home health care?

Medicare may cover certain medically necessary home health services when eligibility requirements are met. Coverage may include skilled nursing care, therapy services, and limited home health aide services related to a covered care plan.

What is a Medicaid waiver program?

A Medicaid waiver program allows states to provide certain long-term care and support services outside traditional institutional settings. These programs often help older adults receive care in their homes or community-based environments rather than in nursing homes.

What happens if a senior runs out of money in a nursing home?

Some individuals may become eligible for Medicaid if they meet state financial and medical eligibility requirements. Medicaid may then help cover ongoing nursing home costs.

Is Medicaid available in every state?

Yes. Medicaid is available in every state, but eligibility requirements, covered services, and available benefits can vary significantly from one state to another.

Can Medicaid take your house?

Medicaid estate recovery rules vary by state. In some situations, states may seek reimbursement for certain Medicaid benefits from a person’s estate after death. Families with concerns about Medicaid planning should consult a qualified elder law attorney or financial professional.

How do seniors qualify for Medicaid?

Eligibility is determined by factors such as income, assets, medical needs, and state-specific requirements. Because rules vary by state, seniors should review their state’s Medicaid guidelines or speak with a benefits specialist for personalized information.

Free Download: Long-Term Care Payment Planning Checklist

Planning for future care can feel overwhelming. Our free checklist helps families organize important financial, insurance, and care information before a crisis occurs.

Download the checklist to help you:

✓ Review Medicare coverage and benefits

✓ Explore Medicaid eligibility and long-term care assistance options

✓ Organize health insurance and prescription coverage information

✓ Identify veterans benefits that may be available

✓ Review financial resources and funding options

✓ Assess current and future care needs

✓ Prepare questions for care providers and benefits specialists

✓ Create a plan before care needs become urgent

Understanding Medicare vs Medicaid Can Help Families Make More Confident Care Decisions

Understanding Medicare vs Medicaid is an important part of planning for future healthcare and long-term care needs. While the two programs may sound similar, they serve different purposes and play distinct roles in helping older adults access care and support.

Medicare primarily helps cover healthcare services such as hospital care, physician visits, preventive care, prescription medications, and short-term rehabilitation. Medicaid, on the other hand, often becomes a critical resource for eligible individuals who need long-term care services, including nursing home care, personal care assistance, and certain home and community-based supports.

As care needs change over time, understanding what each program covers—and what it does not cover—can help families avoid unexpected expenses, explore available resources, and make more informed decisions about future care options.

Whether you are researching assisted living, memory care, nursing homes, home health care, hospice care, or long-term care planning, taking time to learn about Medicare and Medicaid today can help you feel more prepared for the decisions that may arise tomorrow.

Important Information

Every family’s situation is unique. Medicare and Medicaid eligibility requirements, covered services, and long-term care benefits can vary based on individual circumstances and state regulations. Program rules and coverage requirements may also change over time.

The information provided in this article is intended for educational purposes only and should not be considered legal, financial, insurance, or benefits advice. Families should consult appropriate professionals and official government resources when making healthcare, long-term care, or financial planning decisions.